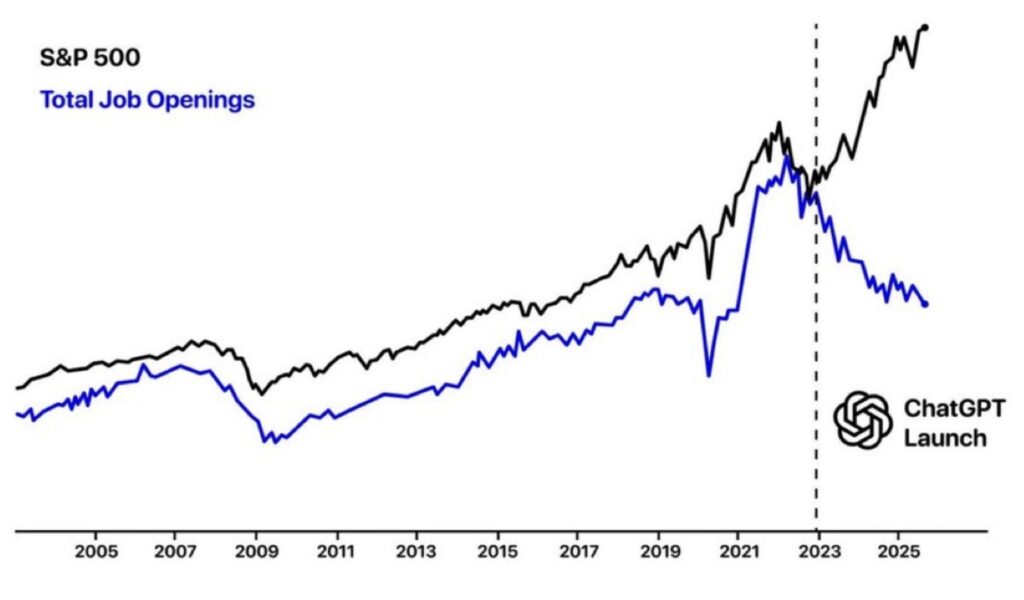

The “Jobless Growth” in One Chart

- Decoupling Dynamics: Post-2022, the S&P 500 has surged while job openings have declined, highlighting a shift toward productivity-led growth driven by AI advancements like ChatGPT’s launch.

- Economic Risks Ahead: This low-fire, low-hire labor market could evolve into a “high firing – no hiring” scenario during the next recession, raising questions about sustained earnings amid softening consumer demand and persistent wage stickiness.

- Broader Implications: While AI, cryptos, and blockchain promise increased global productivity, they risk making jobs redundant, undercutting consumer spending on tech products, and challenging institutions like the Fed to address workforce disruptions—with great power comes great responsibility.

In an era where technological innovation is reshaping the global economy, a striking chart reveals a fascinating yet concerning correlation between the S&P 500 stock index and total job openings in the United States. The graph, spanning from 2007 to 2025, shows the two lines moving in near-perfect harmony until a pivotal moment: the launch of ChatGPT in late 2022. Before this point, economic expansions typically brought rising stock values alongside increased labor demand, creating a symbiotic relationship between market growth and employment opportunities. However, post-2022, we witness a stark decoupling—the S&P 500 continues its upward trajectory, albeit with volatility, while job openings plummet. This visual encapsulates what economists are calling “jobless growth,” a phase where markets thrive on efficiency gains rather than hiring booms. It’s a low-fire, low-hire labor market, where companies are optimizing operations without the need for expansive workforces, potentially setting the stage for more turbulent times ahead.

ChatGPT’s public launch on November 30, 2022, by OpenAI marked a watershed moment in this narrative. Initially based on the GPT-3.5 model and offered as a free research preview through a simple chat interface, it exploded in popularity, surpassing 1 million users in just five days and reaching 100 million by January 2023—making it the fastest-growing consumer application in history. This rapid adoption underscores AI’s transformative power, but the chart’s vertical line at the launch date highlights its immediate ripple effects on the labor market. As AI tools like ChatGPT automate tasks from content creation to customer service, businesses are achieving productivity-led growth without proportional job creation. The S&P 500’s resilience suggests investors are betting on these efficiency gains to boost corporate earnings, even as labor demand cools. Yet, this decoupling raises a critical question: Can these gains sustain long-term prosperity if consumer demand weakens? After all, if AI renders workers redundant, who will be left to buy the latest Amazon gadgets, Tesla vehicles, Apple devices, or Microsoft-powered PCs? In a twist of irony, tech could be undercutting tech itself, eroding the very consumer base that fuels its expansion.

Looking ahead, the low-fire, low-hire environment could morph into something far more precarious—a “high firing – no hiring” reality—especially when the next recession hits. Persistent wage stickiness, where salaries remain elevated despite cooling demand, might exacerbate this, forcing companies to cut jobs aggressively to maintain margins. From a broader perspective, this isn’t just about one chart; it’s a symptom of deeper structural shifts. AI, alongside emerging technologies like cryptos and blockchain, is poised to elevate global productivity to unprecedented heights, powering economies forward. These innovations promise decentralized finance, secure transactions, and automated efficiencies that could redefine industries. However, they also amplify concerns about the future of the workforce. If AI-driven disruptions lead to widespread job irrelevance, the ripple effects could stifle economic vitality. Who benefits when productivity soars but purchasing power dwindles? The S&P 500 may continue trending higher over the long run, navigating volatility through tech-driven gains, but certain jobs—particularly in routine or creative fields—will become obsolete, leaving workers to adapt or face redundancy.

This evolving landscape also prompts scrutiny of institutions like the Federal Reserve (Fed) and its monetary policy. Is the Fed equipped to mitigate the fallout from AI-induced workplace changes? Traditional tools like interest rate adjustments address cyclical downturns, but they may fall short against technological upheavals that fundamentally alter labor dynamics. Change is inherently scary, and the endgame isn’t always clear at the outset. At this moment, it’s challenging to envision AI’s benefits extending beyond corporate cost-cutting and bottom-line growth—benefits that might not trickle down to the broader economy. As we peer into 2025 and beyond, the persistence of wage stickiness could either stabilize or destabilize this fragile balance. I’d love to hear perspectives on how this might unfold: Will efficiency gains from AI sustain earnings, or will they create a feedback loop of reduced consumer spending? Ultimately, as the saying goes, “with great power comes great responsibility.” It’s up to innovators, policymakers, and society to ensure these technologies foster inclusive growth rather than deepening divides.